Buying a home is one of the biggest financial decisions most people will ever make. For many Indiana homeowners and buyers, the mortgage process seems straightforward—until something unusual pops up in the paperwork. If you’ve recently come across the term “anomalous mortgage” in Indiana, you might be wondering what it means, whether it’s a problem, and what you should do next.

You’re not alone. Many property owners discover this term when reviewing property records, refinancing, selling a home, or performing a title search. The good news is that an anomalous mortgage doesn’t automatically mean something is wrong—but it does mean you should understand what’s happening.

In this guide, we’ll break down what an anomalous mortgage is, why it happens in Indiana, how it affects homeowners, and the steps you can take to resolve it.

Table of Contents

What Is an Anomalous Mortgage?

An anomalous mortgage generally refers to a mortgage recorded in property records that appears irregular, unexpected, or inconsistent with the current ownership or financial situation of the property.

In simpler terms, it’s a mortgage entry that raises questions during a title search because it doesn’t align with the normal chain of ownership or financing.

For example, a title company might flag a mortgage as anomalous if:

- The borrower listed on the mortgage is not the current property owner

- The mortgage appears in the records without clear documentation

- The mortgage was recorded incorrectly

- The mortgage should have been released but wasn’t

- The lender information doesn’t match known loan records

These irregularities don’t necessarily mean fraud or legal trouble—but they require investigation before a property transaction can move forward.

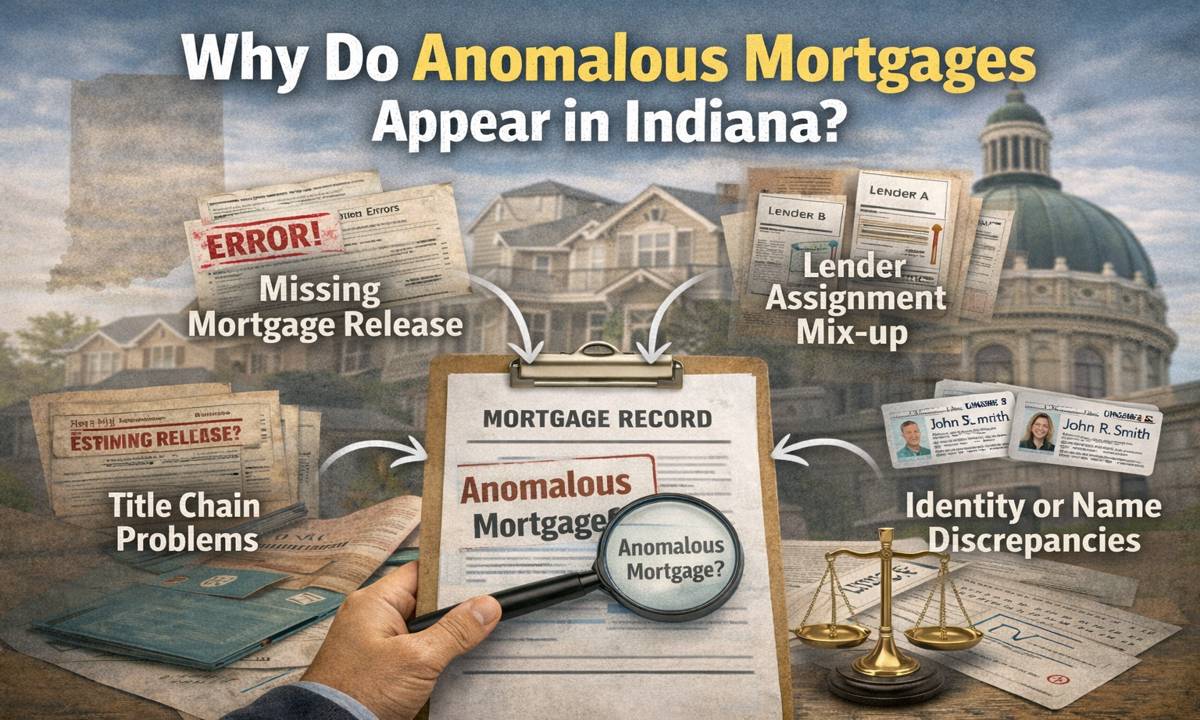

Why Do Anomalous Mortgages Appear in Indiana?

Indiana property records are maintained at the county level, which means documentation accuracy depends on local recording processes. Over time, mistakes, administrative oversights, or incomplete paperwork can lead to anomalies.

Here are some of the most common reasons anomalous mortgages appear.

1. Recording Errors

Sometimes the issue is as simple as a clerical mistake when a mortgage was recorded with the county recorder’s office.

Examples include:

- Misspelled names

- Incorrect property descriptions

- Missing loan details

- Recording the mortgage under the wrong property

Even small errors can create confusion during a title search.

2. Missing Mortgage Release

When a mortgage is fully paid off, the lender typically records a release or satisfaction of mortgage. If that release is never recorded, the mortgage can remain visible in public records.

This is one of the most common causes of anomalous mortgage issues in Indiana.

In reality, the loan may be completely paid—but the paperwork never made it to the county records.

3. Title Chain Problems

Another possible reason is a break or confusion in the chain of title.

For example:

- A previous owner had a mortgage recorded

- The property was sold

- The mortgage was not properly resolved or documented

During a title search, the old mortgage appears unrelated to the current ownership, creating an anomaly.

4. Mortgage Assigned to a Different Lender

Over time, mortgages are often sold or transferred between lenders. When assignments aren’t properly recorded, the paperwork trail can become confusing.

This can lead to situations where:

- The lender on record doesn’t match the current lender

- Mortgage ownership appears unclear

- The loan looks disconnected from the property history

These inconsistencies can be flagged as anomalous.

5. Identity or Name Discrepancies

Sometimes the anomaly is caused by variations in a person’s name.

Examples include:

- Use of middle names or initials

- Married vs. maiden names

- Misspellings in records

While these seem minor, title companies rely on precise records. A name mismatch can make a mortgage appear unrelated to the property.

How Anomalous Mortgages Affect Homeowners

If you discover an anomalous mortgage in Indiana, it usually surfaces during one of these situations:

- Selling a home

- Refinancing a mortgage

- Buying property

- Conducting a title search

- Applying for home equity loans

Because lenders and buyers need clear title, an anomalous mortgage can temporarily slow down a transaction.

Common impacts include:

- Delayed home closings

- Additional paperwork

- Title insurance requirements

- Legal clarification

While it may feel stressful, most anomalous mortgage issues can be resolved once the underlying cause is identified.

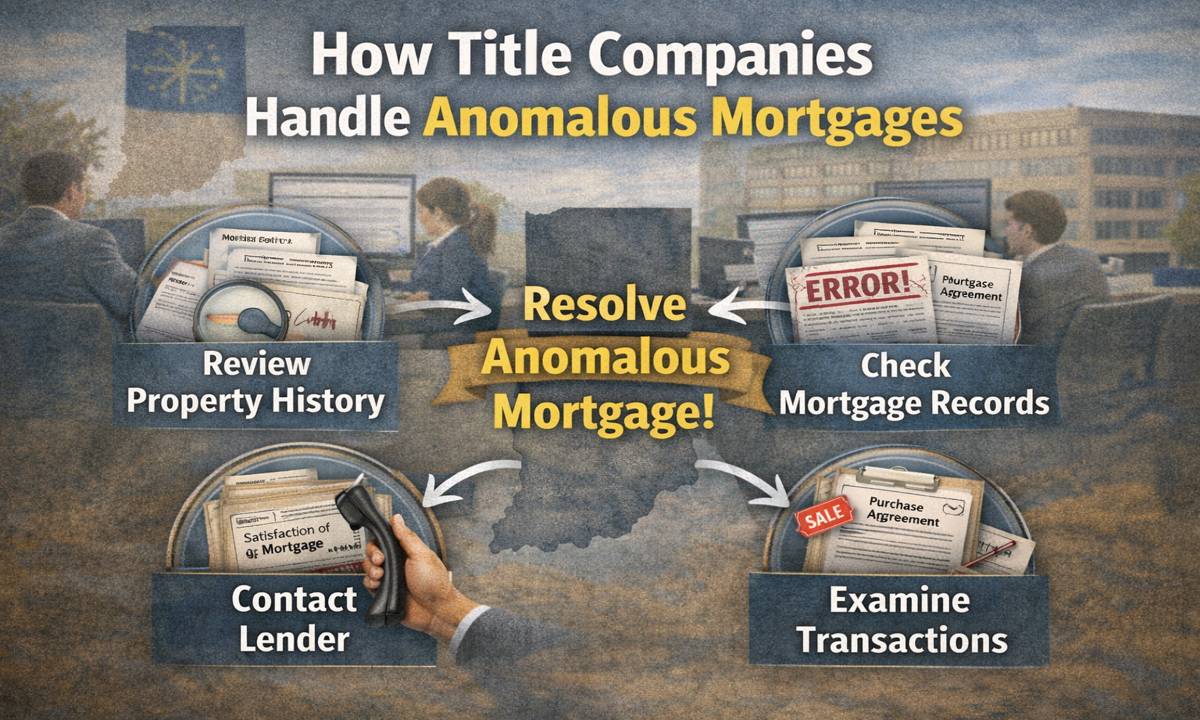

How Title Companies Handle Anomalous Mortgages

When a title company discovers an anomalous mortgage, they typically start by investigating the issue.

This may include:

- Reviewing property history

- Checking mortgage records

- Contacting lenders

- Examining previous transactions

Their goal is to determine whether the mortgage:

- Is valid and still active

- Was already paid off

- Was recorded incorrectly

- Belongs to a different property

Once they confirm the situation, they’ll recommend the next step.

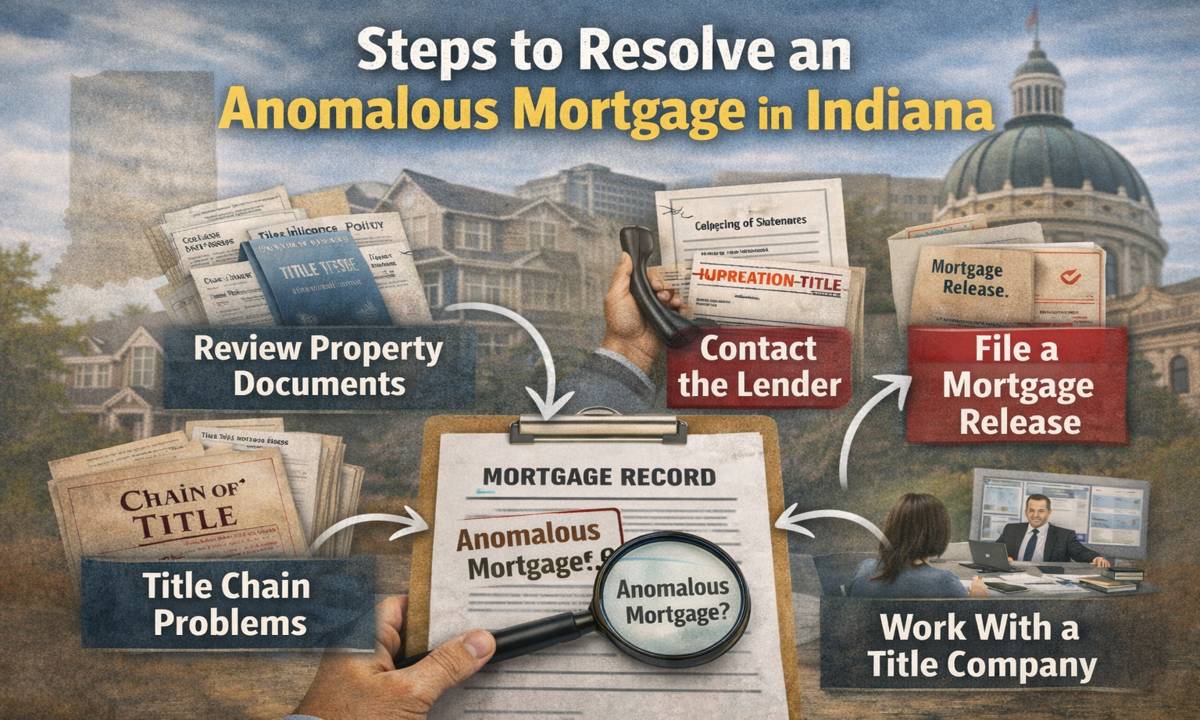

Steps to Resolve an Anomalous Mortgage in Indiana

If you’re dealing with an anomalous mortgage, don’t panic. Most cases are resolved through documentation and verification.

Here are the steps that usually help.

1. Review Your Property Documents

Start by gathering any paperwork related to your property.

This may include:

- Closing documents

- Previous mortgage statements

- Title insurance policies

- Property deeds

These documents often provide clues about the origin of the anomaly.

2. Contact the Lender

If the anomalous mortgage involves a known lender, reaching out directly can clarify the situation.

Ask whether:

- The loan was paid off

- A release was filed

- The mortgage was transferred

In many cases, the lender simply needs to file a mortgage satisfaction document.

3. Work With a Title Company

A reputable Indiana title company can investigate the anomaly and guide you through the solution.

They may assist with:

- Title research

- Documentation gathering

- Filing corrections with the county

- Clearing title defects

Their expertise is especially helpful if you’re in the middle of a real estate transaction.

4. File a Mortgage Release or Affidavit

If the mortgage was paid but not recorded as satisfied, the lender can submit a release of mortgage to the county recorder.

In some situations, a corrective affidavit may be used to clarify the issue.

Once recorded, the anomaly disappears from the title report.

5. Seek Legal Assistance (If Necessary)

Most anomalous mortgages are straightforward to fix, but occasionally the situation is more complex.

If:

- The lender no longer exists

- Records are incomplete

- Ownership disputes arise

You may need a real estate attorney in Indiana to help resolve the issue.

How to Prevent Mortgage Record Issues

While some anomalies are unavoidable, a few simple habits can reduce the chances of problems later.

Keep Important Documents

Always store copies of:

- Mortgage payoff statements

- Closing documents

- Title insurance policies

- Recorded releases

These records can save significant time if questions arise in the future.

Confirm Mortgage Releases

When you pay off a mortgage, confirm that the lender files a satisfaction of mortgage with your county recorder.

You can often verify this online through the county property records database.

Review Your Title Report Carefully

If you’re buying a home in Indiana, review the title report closely before closing.

If something looks unusual, ask questions immediately.

Addressing anomalies early prevents delays later.

Is an Anomalous Mortgage a Serious Problem?

In most cases, an anomalous mortgage is more of a paperwork issue than a legal disaster.

While it may temporarily slow a real estate transaction, it rarely means you’re in financial trouble or at risk of losing your property.

Think of it like a record-keeping hiccup that needs clarification.

Once the proper documents are recorded, the issue typically disappears from future title searches.

Final Thoughts

Encountering an anomalous mortgage in Indiana can be confusing at first. The term sounds technical and even a bit alarming, especially if you’re trying to buy, sell, or refinance a home.

But in reality, most anomalous mortgages are simply the result of missing paperwork, recording errors, or outdated records.

The key is to approach the situation calmly and methodically:

- Review your documents

- Contact the lender if necessary

- Work with a title company

- Record any required corrections

With the right guidance, these issues are usually resolved quickly, allowing your real estate transaction to move forward smoothly.

If you’re currently dealing with an anomalous mortgage, remember—you’re not the first homeowner to run into this situation, and you certainly won’t be the last. The important thing is understanding the issue and taking the right steps to clear your property title.

Tip: If you’re planning to sell or refinance your Indiana home soon, consider requesting a preliminary title search early. It’s one of the easiest ways to catch anomalies before they become last-minute closing surprises.