If you’re a homeowner in Indiana, chances are you’ve heard plenty about refinancing over the past few years. When rates drop, it seems like everyone is talking about locking in something lower. When rates rise, people start wondering if they “missed their chance.”

But refinancing isn’t just about chasing the lowest interest rate. In many cases, it can be a strategic financial move — or a costly mistake — depending on your situation.

So when does refinancing your mortgage in Indiana actually make sense? Let’s break it down in plain English.

Table of Contents

What Is Mortgage Refinancing, Really?

At its core, refinancing means replacing your current home loan with a new one. The new mortgage pays off your existing loan, and you begin making payments on the new terms.

Homeowners in Indiana typically refinance for one (or more) of these reasons:

- To lower their interest rate

- To reduce their monthly payment

- To change the loan term (like switching from 30 years to 15)

- To tap into home equity with a cash-out refinance

- To switch from an adjustable-rate mortgage (ARM) to a fixed-rate loan

But just because you can refinance doesn’t mean you should.

1. When Interest Rates Drop Significantly

This is the most common reason homeowners refinance.

If rates have dropped at least 0.5% to 1% below your current rate, refinancing may be worth exploring. For example, if you currently have a 7% mortgage and you can refinance into a 6% loan, the savings over time could be substantial.

Let’s say you have a $250,000 mortgage:

- At 7%, your principal and interest payment would be about $1,663 per month.

- At 6%, that drops to around $1,499 per month.

That’s a savings of roughly $164 per month — nearly $2,000 per year.

However, you need to consider closing costs. In Indiana, refinance closing costs typically range from 2% to 5% of the loan amount. On a $250,000 mortgage, that could mean $5,000–$12,500.

The key question becomes: How long will it take to break even?

If you’re saving $164 per month and your closing costs are $6,000, you’d break even in about 37 months. If you plan to stay in your home longer than that, refinancing may make sense.

2. When You Want to Lower Your Monthly Payment

Sometimes it’s not about the interest rate — it’s about breathing room in your budget.

If your financial situation has changed (job transition, new baby, medical expenses, etc.), refinancing into a longer-term loan can lower your monthly payments.

For example:

- Moving from a 15-year mortgage to a 30-year mortgage

- Resetting your 30-year mortgage after 10 years back into a new 30-year term

Yes, you may pay more interest over time. But if it helps stabilize your finances now, that trade-off might be worth it.

For many Indiana homeowners — especially in areas like Indianapolis, Fort Wayne, or Evansville where housing remains relatively affordable compared to national averages — keeping monthly costs predictable is a major priority.

3. When You Want to Pay Off Your Home Faster

On the flip side, refinancing can help you get out of debt sooner.

If your income has increased or you’re in a stronger financial position, switching from a 30-year mortgage to a 15-year loan can:

- Reduce your interest rate

- Save tens of thousands in long-term interest

- Help you build equity much faster

The monthly payment will likely increase, but the long-term savings can be dramatic.

This strategy works best if:

- You have stable income

- You have a strong emergency fund

- You’re confident you can handle the higher payment

4. When You Want to Tap Into Your Home’s Equity

Indiana home values have appreciated in many markets over the past several years. If your home is worth significantly more than when you purchased it, you may have built up meaningful equity.

A cash-out refinance allows you to borrow against that equity and receive the difference in cash.

Homeowners often use this money for:

- Home renovations

- Paying off high-interest credit card debt

- Covering college tuition

- Starting a business

For example, if your home is worth $300,000 and you owe $180,000, you may be able to refinance into a $220,000 loan and take $40,000 in cash (depending on lender limits).

But this strategy comes with risk. You’re turning unsecured debt (like credit cards) into secured debt tied to your home. If you can’t make payments, your house is on the line.

Cash-out refinancing makes the most sense when:

- You’re consolidating high-interest debt responsibly

- The money is being used to increase the home’s value

- You have a solid repayment plan

5. When You Want to Get Rid of Mortgage Insurance

If you purchased your Indiana home with less than 20% down, you’re likely paying private mortgage insurance (PMI).

As your home’s value increases and your loan balance decreases, you may now have 20% equity or more.

Refinancing could eliminate PMI, potentially saving you $100–$300 per month depending on your loan size.

Before refinancing, however, check whether you can remove PMI through a new appraisal without refinancing. Sometimes that’s the simpler and cheaper route.

When Refinancing Does Not Make Sense

Refinancing isn’t always the smart move.

It may not make sense if:

- You plan to sell your home within the next few years

- Your credit score has dropped significantly

- Closing costs outweigh potential savings

- You’re extending your loan term and increasing long-term interest dramatically

Also, if rates are higher than your current mortgage rate, refinancing purely for a lower payment rarely makes sense unless you’re restructuring debt strategically.

Indiana-Specific Considerations

Indiana is known for relatively low property taxes compared to many states, but they can still vary by county. When refinancing, your escrow setup may change slightly, so be prepared for possible adjustments in your monthly payment.

Additionally, local housing markets matter. Home values in areas like Carmel, Fishers, and parts of Northwest Indiana may differ significantly from rural counties. Your home’s appraised value will impact your refinance options.

Working with a lender familiar with Indiana’s market conditions can make the process smoother.

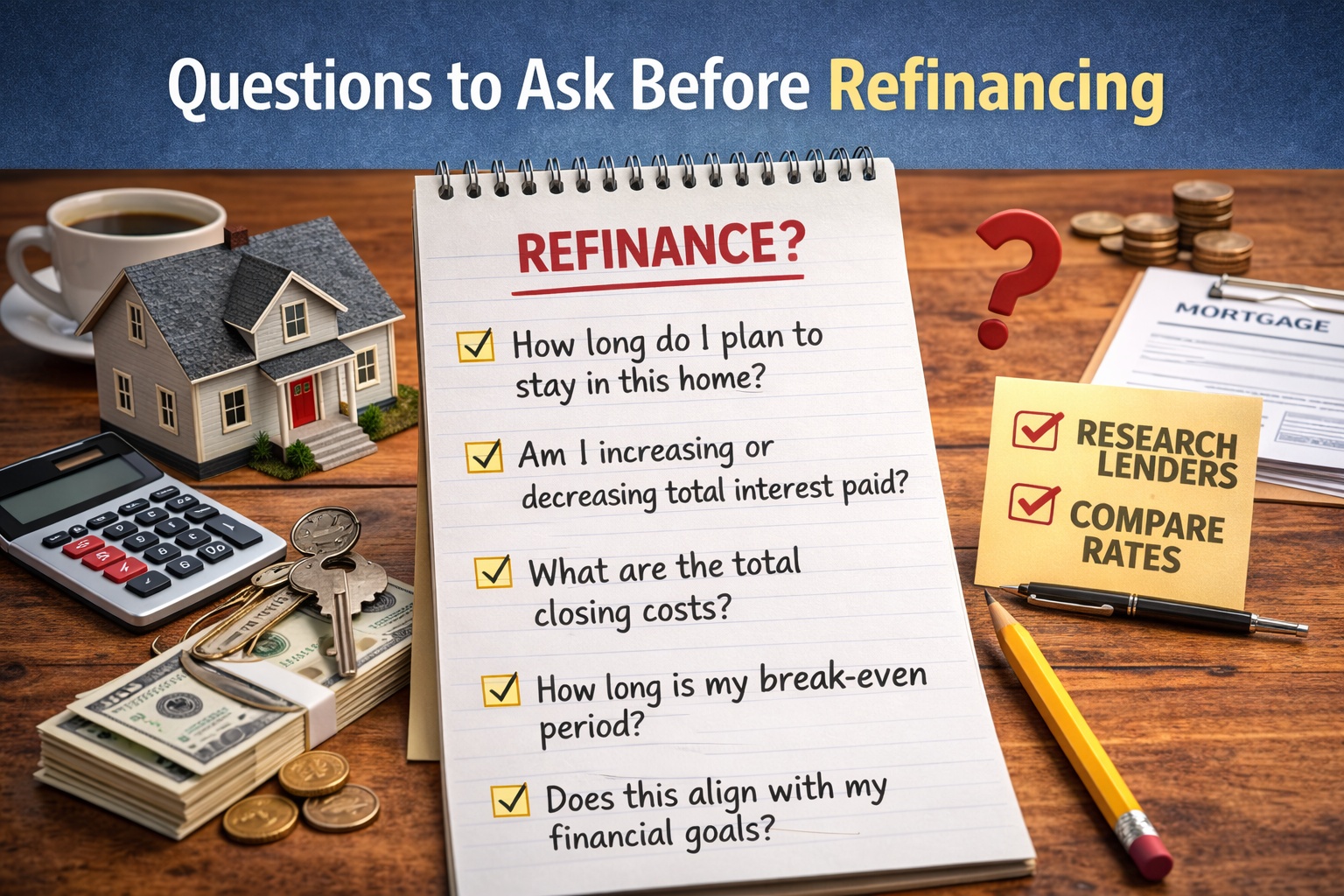

Questions to Ask Before Refinancing

Before signing anything, ask yourself:

- How long do I plan to stay in this home?

- What are the total closing costs?

- How long is my break-even period?

- Am I increasing or decreasing total interest paid over time?

- Does this move align with my long-term financial goals?

Refinancing should support your broader financial plan — not just offer short-term relief.

Final Thoughts

Refinancing your mortgage in Indiana can absolutely make sense — but only under the right circumstances.

If you can significantly lower your interest rate, remove PMI, pay off your home faster, or strategically use equity, refinancing can strengthen your financial position.

However, if the math doesn’t work, or if you’re planning to move soon, it may be better to stay put.

The key is running the numbers carefully and thinking long term. A refinance isn’t just paperwork — it’s a reset of one of the biggest financial commitments in your life.

When done thoughtfully, it can be a powerful tool. When done impulsively, it can cost you.

As with most financial decisions, the smartest move is the one that fits your goals — not just the headlines.